The Brent crude price has dropped as much as two-thirds from its high in June 2014 to $37.89 per barrel. For a country that imports a huge portion of its oil requirements, this phenomenon has been a blessing for India.

How much did we gain?

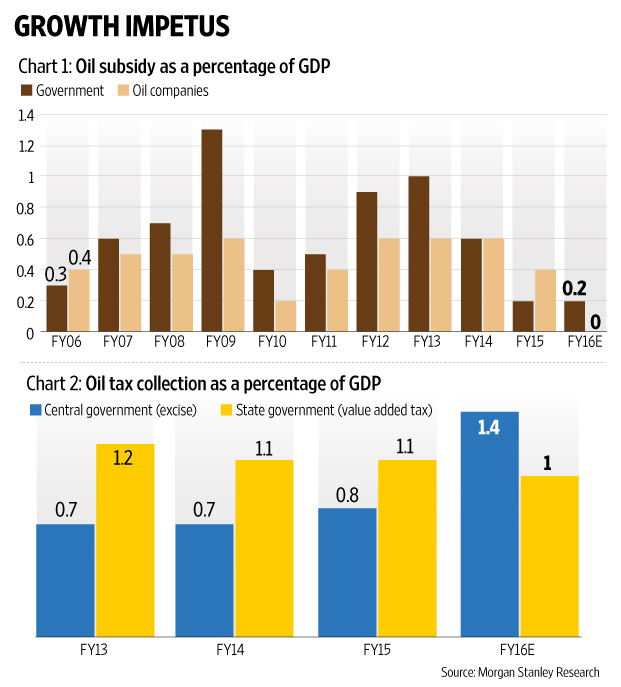

Firstly, the lower oil prices means under-recovery (or losses from selling fuel below cost) for the sector will drop. As chart 1 alongside shows, Morgan Stanley Research expects the government’s oil subsidy burden to be 0.2% of gross domestic product (GDP) in fiscal 2016. While that is the same ratio as in FY15, it has dropped substantially from a high of 1% of GDP in FY13. At the same time, the subsidy burden borne by oil companies is expected to drop sharply.

Secondly, as this column has pointed out before, the drop in the retail prices of diesel and petrol has not been commensurate with the drop in broader crude prices or the Indian basket of crude. Retail prices have fallen at a slower pace, as the government has hiked excise duty on petrol and diesel six times since November 2014. Chart 2 shows the gains to the central government on account of excise since FY13. However, the states are likely to lose some revenue, given the ad valorem nature of the state-level value added tax on petroleum products, says Morgan Stanley.

Even though the retail prices haven’t fallen as much, the Indian consumer cannot complain. Based on the savings from the lower prices of petrol and diesel (used by households), Morgan Stanley estimates households have gained directly approximately $8 billion, or ~0.5% of GDP, from falling crude oil prices since FY13. Additionally, some indirect benefits, too, are expected as corporates could have passed on the gains to consumers in the form of lower product prices. Corporates, too, would have benefitted. “We believe the corporate sector has largely used the oil gains to improve balance sheets and pass on some benefits to consumers as private corporate capex has continued to be weak,” pointed out Morgan Stanley.

So far so good. What next? The way ahead may not be that smooth.

“If crude oil prices were to rebound sharply, the government may be forced to partly roll back the increases in excise duty on diesel and gasoline effected in FY15 and FY16, which has contributed meaningfully to the (fiscal) improvement seen in the past two fiscal years,” wrote analysts from Kotak Institutional Equities in a note to clients on 10 December.

Commenting on the mid-year economic review, Nomura Research economists said the government expects fiscal 2017 outlook to be challenging due to (a) the additional fiscal burden on account of the seventh pay commission (~0.65% of GDP) and the “one rank one pension” scheme; (b) lower nominal GDP growth, which could hurt revenue collection; (c) the need to continue to increase public investment in infrastructure to offset weakness in private demand; and (d) the gains from lower oil prices (on subsidy) may not be sustained.

Simply put, it is unlikely that the benefits from the drop in crude prices will provide the same boost to growth in 2016.